- Home /

- Achievements and forecasts /

- Business environment

- LOTOS Annual Report 2011 /

- Home /

- Achievements and forecasts /

- Business environment

Business environment

2011 brought an increase in geopolitical risks stemming from the regions which are major global oil suppliers.

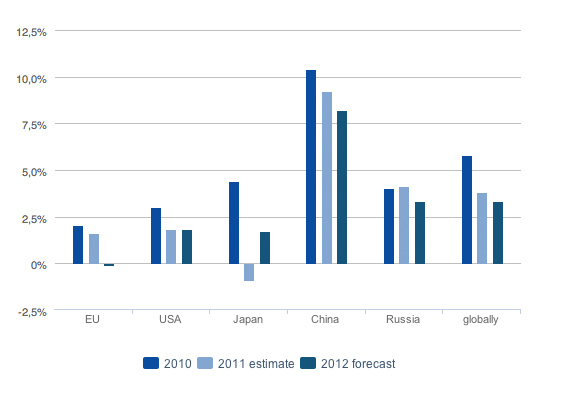

GDP growth in 2010 and 2011 (year-on-year change) (%)

Source: In-house analysis based on Eurostat, OECD, and MFW data.

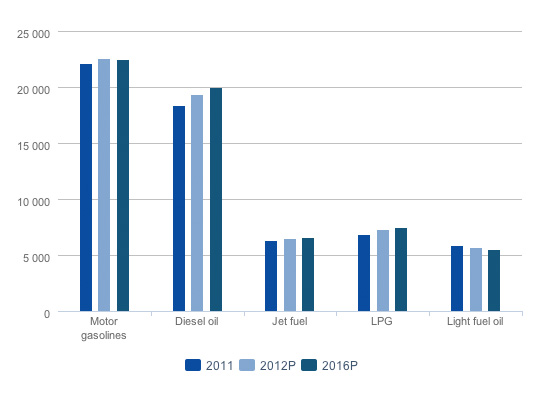

Global consumption of fuels (thousand b/d)

Forecast global consumption of fuels (thousand b/d)

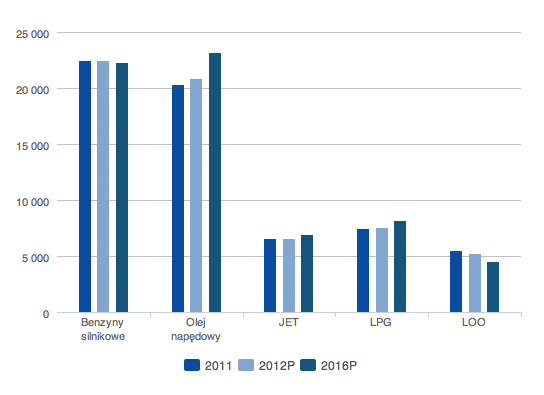

Forecast consumption of fuels in Europe (thousand b/d)

PAGE CONTENTS

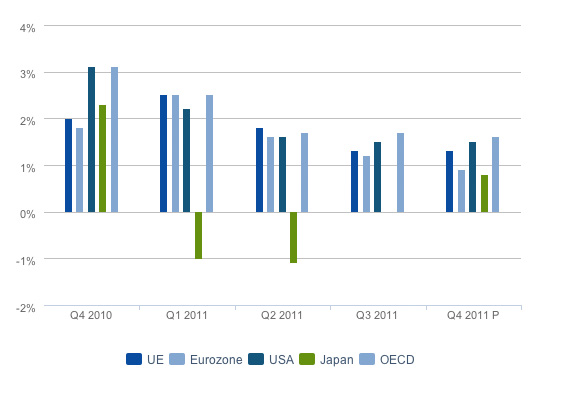

The economic situation in 2011 was worse than expected. The largest world economies retained growth in the positive territory, but growth rates were lower than a year earlier. The key decelerating factors included slower recovery of retail demand in developed countries and the return to financial instability, particularly in the European markets.1

2011 was predominated by the sovereign debt crisis spreading in Europe. Rescue plans were implemented, often encountering strong social protests. Speculations abounded, both among economists and publicists, concerning a potential break-up of the eurozone, or even of the entire European Union. This uncertainty had a negative impact on the development prospects of the global economy. And there was the natural disaster - the earthquake and tsunami in Japan - which came as a blow to many markets, including the petroleum market.

There were also some significant geopolitical changes, entailing conflicts and unrest in North Africa, a region with a significant crude oil production potential. Social unrest and rebellions, e.g. in Saudi Arabia, Egypt, Syria, Yemen, Kuwait, and Nigeria have sparked serious concerns about disruptions of crude oil supplies to Europe. The revolt which led to a civil war in Libya reduced the supplies of crude from this country. The effects of limited production from Libyan oil fields will continue to be felt for a long time. The International Energy Agency (IEA) estimates the aggregate drop in oil production in Libya, Syria and Yemen in 2011 at approximately 450 million barrels2. This shortfall in supplies was partly offset through a release of IEA reserves. According to the Agency, the effects of the Libyan uprising would have been more acute if it were not for the economic crisis and limited demand for the commodity in Europe.

In the closing weeks of 2011 Iran, which pursues its own nuclear programme, emerged as another trouble point. The build-up of the conflict around the potential closing of the Strait of Hormuz, which concentrates a vast share of the global seaborne oil shipments, the possible EU embargo on Iranian crude and the risk of an armed conflict between Israel and Iran all sent oil prices soaring.

The geopolitical risks stemming from the regions which are major global oil suppliers lifted the average Dtd Brent prices in 2011 to a historical high of 111.5 USD/bbl (compared with 79.5 USD/bbl in 2010). Combined with a depreciation of the złoty against the dollar, the high prices of the commodity pushed fuel prices at Polish service stations to new historical highs.

But more than by anything else, the problems of the eurozone may become the most serious deterrent to the global economic recovery. The eurozone's problems are visible already in estimates of the 2011 GDP growth rate, which amounted to 3.8% for the global economy (0.2pp below September 2011 forecasts). The forecast for 2012 has been affected by a stronger downward correction (of 0.7pp), which has set the expected GDP growth rate at 3.3%. The new forecast takes into account a shallow recession (of -0.1% GDP) in the European Union3.

To overcome the economic problems in developed countries, reforms of budgetary policies will be needed in order to eliminate the financial imbalance in the public sector. This restricts the governments' ability to intervene in the real economy.

1 World Economic Outlook, International Monetary Fund, September 2011.

2 Oil&Gas Journal, January 2012.

3 World Economic Outlook Update, January 2012.

Condition of the refining industry

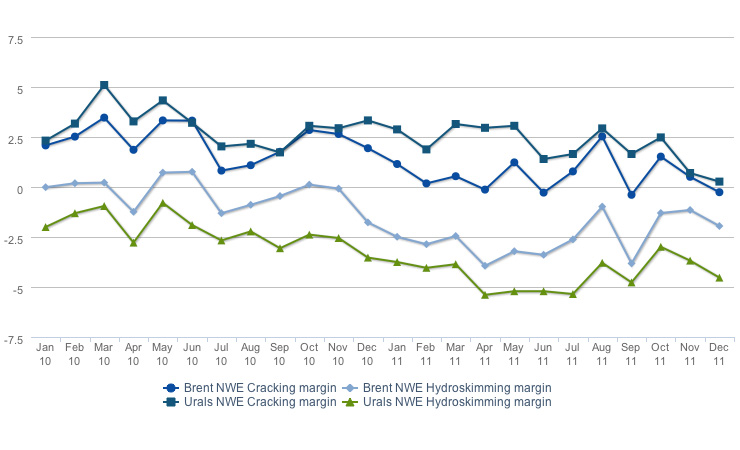

Due to the economic problems in Europe, the refining margins in the region were on a decline. In the first half of 2011, those refineries which could purchase and process Urals crude, enjoyed an additional premium on the Brent/Urals differential. However, in the second part of the year the differential was almost to zero, closing the gap between the margins generated by refineries processing Urals crude and the margins relying on Brent as the reference crude.

The difficult situation on the European refining market affected chiefly those refineries which are technologically less advanced (hydroskimming), and which produce less high-value-added fuels from crude than modern facilities (cracking). Many of the hydroskimming refineries generated negative margins. In late 2011, this negative tendency found its confirmation in the form of financial distress experienced by Petroplus, an independent refiner operating several refineries in Western Europe.

Gasoline was the product with the most volatile margins in 2011. It started the year with strong increases, but close to its end the refining margin contracted close to 0 USD/bbl. Gasoline reacts faster than other fuels to price changes or changes in the economic climate and financial situation of consumers. What is more, the European refining industry suffers from a structural excess of gasoline distillates. High supply of gasolines, combined with increasingly more limited possibilities to export them to the American continent, had a negative effect on the margins.

Margins on middle distillates, particularly on diesel oil, remained stable. Middle distillates are the group of products enjoying the highest demand in Europe, and stayed strong even in spite of the economic uncertainty. Another noteworthy development was the strengthening of margins on heavy fuel oil, seen close to the end of the year on the back of the introduction of new fiscal policies in Russia and the resulting drop in supply of the product from the East.

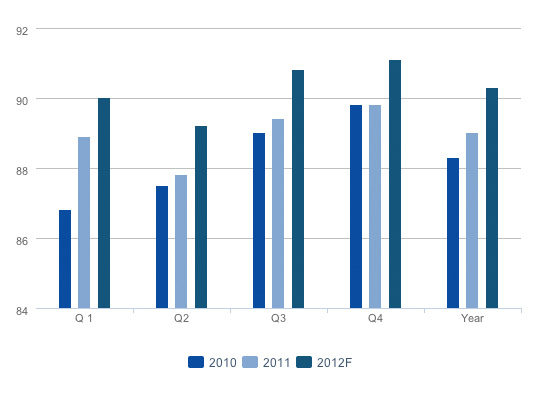

The economic growth seen in 2011 contributed to higher consumption of crude oil. There was an overall increase in demand for crude oil, especially due to higher consumption on the developing markets4, as well as an increase in crude prices. Industry organizations are estimating average demand for the commodity in 2011 at 88.3 mb/d, which is about 1% (0.9 mb/d) more than a year earlier. At the same time, average consumption of crude in 2012 is expected to come in at 89.5 mb/d, up by 1.3%5. Medium-term forecasts by the International Energy Agency predict that demand for crude will reach 95 mb/d in 2016, meaning a compound average growth rate (CAGR) of 1.3%.

IEA estimates indicate that the global growth is driven by rising demand for the commodity in developing countries. In 2011, the growth in non-OECD countries was 1.2 mb/d, and it may accelerate to 1.6 mb/d in 2012. Concurrently, consumption in developing countries fell by 0.5 mb/d (2011), and may decline by a further 0.3 mb/d in 2012.

Estimated demand for crude in Europe was 15 mb/d in 2011, against a forecast 2012 consumption figure of 14.8 mb/d.6

4 Oil Market Report, IEA, December 2011.

5 In-house compilation based on OPEC, IEA and US EIA data.

6 Oil Market Report, IEA, December 2011.

International fuel market7

It is estimated that demand for oil refining products rose in 2011 by 1.2% globally. An increase in demand was seen primarily in the diesel oil and LPG segments (up by 3.3% and 2.3%, respectively), while consumption of engine fuels remained stable (down by 0.2%). Consumption of light fuel oil fell again (down by 2.8%). These changes in global consumption of fuels came as a result of the weak economic growth.

According to forecasts, global consumption of refining products is expected to grow by 6% until 2016. Relative to 2011, demand for diesel fuel and LPG is expected to surge by 14% and 10%, respectively. Consumption of gasolines may decline by a little short of 1%. A drop in consumption of light fuel oil (-17%) is also predicted.

Demand on the European market is expected to fall in 2011 by 0.8%. Higher consumption was recorded only with respect to middle distillates. Consumption of diesel fuel rose by 0.6%, and demand for JET fuel - by 1.2%. Consumption fell in the case of motor gasolines (-3.6%), LPG (-0.4%) and light fuel oil (-4.4%).

By 2016, demand for refining products in Europe is expected to fall by 3.2%, which will mostly be attributable to a considerable (over 13%) decline in consumption of gasolines. At the same time, demand for middle distillates is expected to grow significantly, by 6.4% in the case of diesel oils and by 2.0% in the case of jet fuel.

In the European car market, new passenger car registrations fell slightly (by 1.4%) in 2011, to 13.6m new cars, whereas in the utility vehicles segment new registrations rose by 10%, to 2m vehicles. In the group of registered new passenger cars, an increasing interest in diesel fuelled cars was visible. In Q1 2011, the share of such cars in the total new car registrations was 55%, compared with 52% in 2010 and 46% in 2009.

7 Mid-Term Oil Market Outlook 2011-2016, JBC Energy, October 2011.

8 European Automobile Manufacturers’ Association.

Poland – macroeconomic environment

In 2011, the Polish economy recorded a good economic performance. Real GDP growth was 4.3% (against 3.9% in 2010) on higher internal consumption and investments. Last year's average annual inflation was 4.3%.

There were also positive signals from the labour market, where employment was up by 3.2%, and salaries in the non-financial corporate sector rising by 5%. At the end of 2011, unemployment was 12.5%, staying relatively flat over the previous year's figure.

Polish fuel market

In 2011, the Polish economy was in the growth phase of another economic cycle. According to initial estimates by the Central Statistics Office, GDP grew by 4.3%. Internal demand recovered (up by 3.8%), and investment projects (up by 8.7%) that had been postponed in the previous years now stimulated the economy.

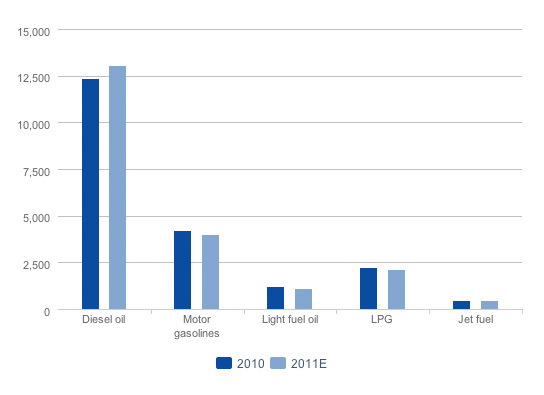

The good economic conditions prevailing in the country throughout 2011 had a positive impact on demand for transport services and on growing capacities of the transport sector, contributing to stronger demand for diesel oil, the key fuel used in transport. In 2011, demand for diesel oil exceeded 13.3m tonnes, and was up year on year 8%.9

Growing demand for diesel oil, combined with such factors as increasing dieselisation of the market and price volatility on the global petroleum markets, resulted in a drop of demand for gasoline and a nearly 5% lower consumption of this fuel in 2011 relative to 2010 (4m tonnes in 2011). Similar trends in fuels consumption were observed across all of Europe.

In parallel with the drop in demand for gasoline, there was a 4% decline in consumption of LPG, which fell from 2.2m tonnes in 2010 to approximately 2.1m tonnes in 2011. There was also a decline in consumption of light fuel oil, which fell in 2011 mainly due to a relatively warmer winter close to the end of the year and due to permanent changes in heating fuel consumption patterns. Demand for light fuel oil fell by 11%.

In aggregate, demand for liquid fuels, including diesel oil, gasoline, LPG and light fuel oil, rose by 2.9% relative to 2010, on the back of high consumption of diesel oil and a dynamic development of this market segment.

Economic forecasts for Poland are fairly optimistic, so the economy's good performance may be expected to stimulate demand for fuels in the following years. According to forecasts, demand for fuels should be growing at an annual rate of about 3%.

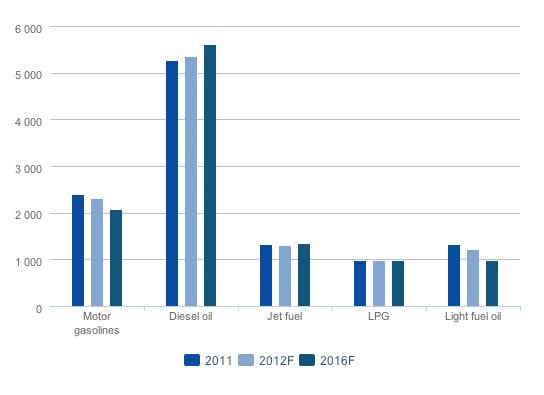

Owing to the increased number of airline passengers and aviation operations, in 2011 demand for jet fuel rose by 3% year on year. Prospects for jet fuel for the following years are good – higher air passenger traffic in connection with the Euro 2012 championships and the growing mobility of Poles as they become increasingly wealthier provide grounds to expect future consumption of this fuel to grow by about 5% a year.

9 Estimates based on the Polish Organisation of Oil Industry and Trade (POPiHN) data.

Retail fuel market in Poland

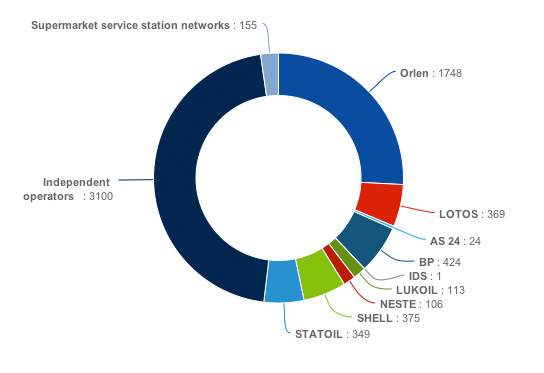

2011 saw further consolidation of the retail segment and optimisation of the service station chain. At the end of the year, there were 6,764 service stations operating on the Polish retail fuel market, a number similar to the 2010 figure.

Data show that there was a drop in the number of service stations owned by independent operators, while in the case of large Polish and foreign chains the numbers rose. There were also some changes in the segment of motorway service stations. At the end of the year, there were 38 such stations in Poland, operating as Motorway Service Areas. This market segment is expected to grow further over the next few years.

Important events in the retail market in 2011 include the launch of a new brand in the economy segment - LOTOS Optima. At the end of the year, there were 50 service stations operating under this brand.